We all feel the anxiety that comes with fluctuating financial markets. Interest rate fluctuations can seem overwhelming, and without a grasp on what they mean, your financial planning and wealth growth can take a hit. I’ve spent years analyzing these market dynamics, and I want to share that insight with you.

Understanding these changes is key. You can’t afford to ignore them if you want to build and preserve wealth. This article will break down interest rate fluctuations, explaining their causes and effects in clear terms.

You’ll get actionable strategies for managing your finances wisely, regardless of how the market shifts. I aim to equip you with a practical system for making informed decisions that lead to wealth building.

If you’re ready to take control of your financial future, Together, we’ll demystify this complex topic and set you up for success.

Mastering Interest Rates: What You Need to Know

Interest rates. Sounds boring, right? But they’re the backbone of finance.

Essentially, they’re the cost of borrowing money or the reward for lending it. When interest rates fluctuate, it’s like the stock market’s wild cousin, always moving up or down.

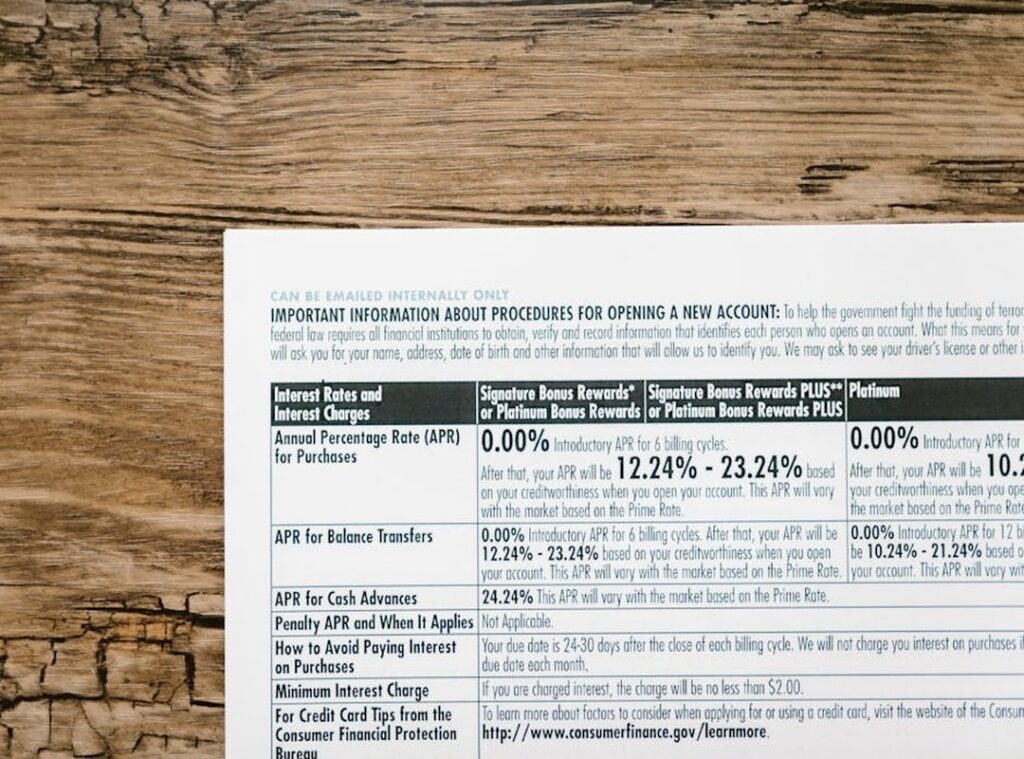

You see these fluctuations everywhere: in your mortgage, savings account, or credit card interest. Ever wonder why your credit card seems to charge more some months? That’s interest rate fluctuations playing their part.

Understanding these changes is key for building wealth. Think of it like navigating through Hogwarts. Exciting, but tricky.

You need to know which spell (or rate) might change next and why.

If you want financial stability, grasping these variations is important. Otherwise, you might as well throw your money into a black hole. So, are you ready to dive deeper into how interest rates affect your financial life?

It’s time to start paying attention.

The Real Deal on Interest Rate Fluctuations

Central banks, like the Federal Reserve, wield enormous power over interest rates. They set the federal funds rate (a key tool) to guide economic stability. This isn’t just some arcane financial wizardry.

It’s the bedrock of economic plan. Does it always make sense? Not really.

Inflation is the usual suspect here. When prices soar, interest rates often follow suit, as central banks try to cool things down. But is hiking rates always the answer?

Maybe not.

Economic growth plays a major role too. A strong economy can drive rates up, while a weak one may see them drop. It’s a balancing act, and frankly, it doesn’t always work out.

Then there’s the supply and demand for credit. More demand? Rates might rise.

And let’s not forget government debt and global economic conditions. These can really shake things up. It’s all interconnected, like a financial web (or a soap opera).

Too much supply? They could drop. A game of tug-of-war that doesn’t always have a clear winner.

If you’re curious about the future cryptocurrencies finance, this kind of economic backdrop matters. It’s a fascinating (and sometimes frustrating) world we live in.

How Interest Rates Shape Your Finances: The Real Deal

Interest rate fluctuations can shake up your finances. When rates rise, borrowing becomes pricier. I mean, have you checked your mortgage rate lately?

Variable rates can skyrocket, making your monthly payments a headache. Credit card interest? It eats away at your wallet, too.

Personal loans aren’t spared either. So, if you owe money, higher rates aren’t your friend.

But there’s a silver lining. Got savings? Higher rates can boost your savings account returns.

CDs and money market funds become attractive again. Remember the last time they were this appealing? Probably not.

But don’t get too excited. Lower rates can slash these returns, leaving your savings stagnant.

Bonds have their own story. When rates go up, bond prices fall. It’s like a seesaw.

This inverse relationship is key for those holding fixed-income portfolios. Understand this changing, and you can get through the bond market better.

Now, let’s talk stocks. Higher rates can make borrowing costlier for companies. Bonds might look better than stocks, affecting equity valuations.

Real estate isn’t immune either. Interest rate changes impact mortgage affordability, demand, and property values. Want to dive deeper into these dynamics?

Discover more on understanding economic bubbles impact. Keeping an eye on rates is more than just numbers (it’s) about safeguarding your wealth.

Interest Rate Swings: Strategies for Survival

Interest rates can be a wild ride. I’ve learned that the hard way. When rates climb, variable-rate debt feels like a tightening noose.

You know what I mean, right? If you’re in this boat, consider accelerating payments. Paying more now can save you loads later.

Better yet, look into refinancing to a fixed rate if possible. It’s not glamorous, but it’s smart.

Now, let’s talk about savings. When rates are favorable, don’t let your money sit idle. Explore high-yield savings accounts or Certificates of Deposit (CDs).

They might seem boring, but they’re reliable earners when interest rates are on the up. And when they drop? Adjust accordingly.

Flexibility is key.

Diversification is your friend. Spread your investments across different asset classes. Stocks, bonds, real estate, even commodities.

It’s the best way to buffer against interest rate fluctuations. I learned this lesson after putting all my eggs in one basket and watching rates flip everything upside down. Don’t make my mistake.

Choosing between fixed and variable rates for loans? That’s tricky. Fixed rates offer stability, while variable rates can save you when rates are low.

It’s a gamble, often linked to personal risk tolerance.

Finally, keep your eyes on the long-term prize. Short-term rate swings shouldn’t derail a well-planned investment plan. Rebalance your portfolio periodically.

Maintain your desired asset allocation despite market shifts. Staying proactive in response to changes is key. Trust me, in the long run, it pays off.

Foreseeing and Adapting: Key Indicators to Watch

When it comes to building wealth, interest rate fluctuations are like the weather. You can’t ignore them. Inflation reports, like CPI and PCE, are key.

They tell us how fast prices are rising, which affects everything from groceries to mortgages. It’s a reality check. Employment data, with jobless claims and unemployment rates, shows us the health of the job market.

More jobs usually mean a healthier economy.

Then there’s GDP growth. It’s the pulse of economic activity. But don’t stop there.

Central bank communications are like treasure maps. Their statements and speeches reveal future monetary policy moves. Miss them, and you’re in the dark.

Bond yields, especially the yield curve, are whispers of the economic future. They hint at upcoming interest rate changes. Are you listening?

Staying informed through reputable financial news sources is not optional. It’s important. Expert analysis can decode these cryptic signals for us.

It’s like having a financial GPS.

Proactive monitoring isn’t just smart. It’s necessary. It enables timely adjustments to our financial strategies.

We need to align with the market, not fight it. This is prudent wealth-building. It’s not just about watching.

It’s about acting when the time is right.

Take Charge of Your Financial Future

Understanding interest rate fluctuations isn’t just for the experts. It’s important for everyone who wants to take control of their finances. Too many people feel helpless against the financial markets.

You don’t have to be one of them.

The takeaways I’ve shared offer a clear path for understanding and adapting your financial plans to rate changes.

Now is the time to act. Review your current financial products. Consult with a financial advisor who can tailor strategies that fit your goals.

Don’t let uncertainty hold you back. Take charge today to help your financial future.

Founder & Chief Executive Officer (CEO)

Eldrin Selmorne is the visionary founder of Xuirme Jets, shaping its direction as a finance intelligence and strategy platform. With a strong background in financial systems and investment thinking, he leads the company’s long-term vision and growth strategy. As CEO, he oversees operations, partnerships, and innovation, ensuring the platform delivers high-value insights and actionable financial knowledge.

Founder & Chief Executive Officer (CEO)

Eldrin Selmorne is the visionary founder of Xuirme Jets, shaping its direction as a finance intelligence and strategy platform. With a strong background in financial systems and investment thinking, he leads the company’s long-term vision and growth strategy. As CEO, he oversees operations, partnerships, and innovation, ensuring the platform delivers high-value insights and actionable financial knowledge.