Interest rate changes can feel like a tidal wave crashing over your finances. Many people don’t really understand what these adjustments mean for their money. I get it.

It’s confusing and can lead to anxiety about budgeting, saving, and debt management.

With years of experience in financial analysis and market observation, I see these shifts clearly. I’ve tracked how they impact everyday lives, and trust me, they do. You need to know how interest rates changes affect you personally.

This article will break it all down. I’ll provide clear definitions and practical insights. You’ll get actionable steps to handle these changes.

My goal is to help you to make smart financial decisions. You won’t be left in the dark anymore. I’ll guide you through the complexities of interest rates so you can confidently manage your finances.

Let’s dive in.

Interest Rates: The Basics You Need to Know

Let’s keep it simple. An interest rate is just the cost of borrowing money or the reward for saving it. That’s it.

When you hear about “interest rate adjustments,” we’re talking about changes to a country’s benchmark interest rate. Usually, this is handled by the central bank (like the Federal Reserve in the U.S.).

Why do they mess around with these rates? Well, central banks have a few big goals: keeping inflation in check, promoting economic growth, and making sure stable employment. They watch economic indicators like inflation rates, unemployment figures, and GDP to make these calls.

Picture the central bank as a thermostat for the economy. They tweak rates up or down to keep things balanced.

Now, let’s get a bit opinionated here. I think these adjustments are key (not to use a banned word, but come on, they are). Sure, some folks argue that constant rate changes can create uncertainty.

But without them, controlling inflation would be like steering a ship without a rudder.

Speaking of the future, ever wonder how future digital currencies might play into all this? It’s a fascinating thought. As we move towards more digital financial systems, the way we think about interest rates might shift too.

But for now, those good ol’ interest rate changes are here to stay. They keep our economic engine running smoothly, and honestly, I wouldn’t have it any other way.

Your Wallet’s First Stop: Impact of Rate Changes on Loans

Let’s talk about how interest rates changes can mess with your loans. Mortgages come in two flavors (fixed-rate and adjustable-rate (ARMs). Fixed-rate mortgages sit tight no matter what.

ARMs? They dance to the rate beat. When rates rise, your ARM payments might climb.)

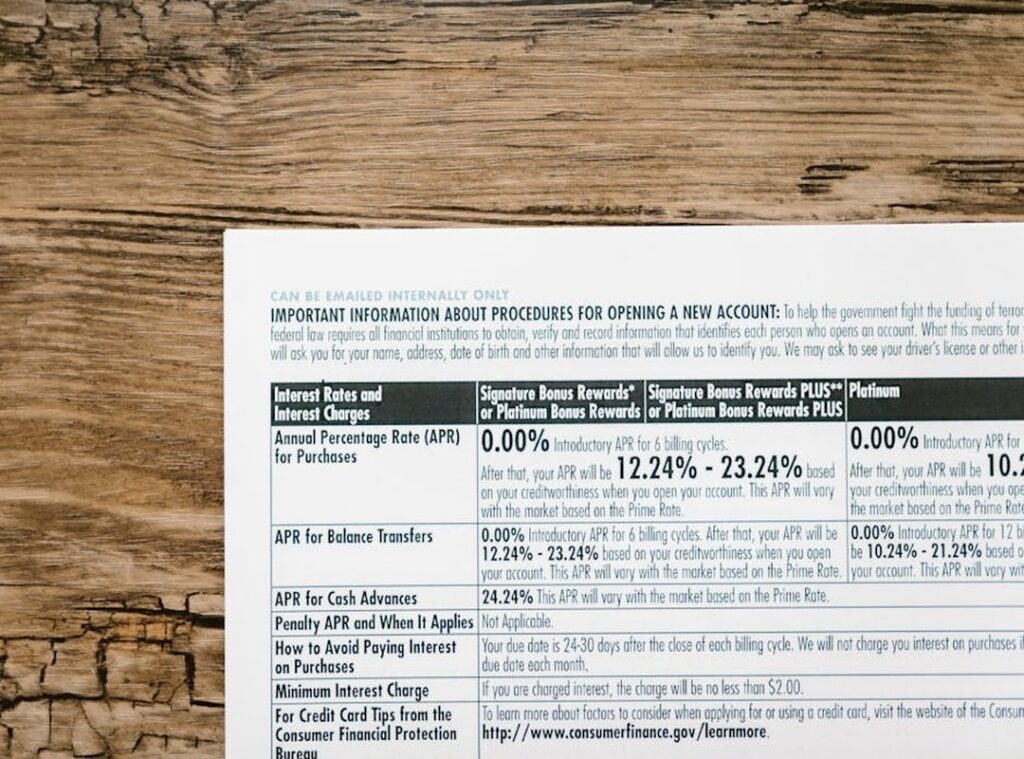

Now, credit cards. Most have variable rates, so your APR can change if you carry a balance. That means your monthly payments might jump.

Just what you needed, right?

So, it’s important to know what you have.

Auto loans and personal loans? New loans feel rate shifts. Fixed loans won’t budge, but variable ones will.

Here’s some advice for when rates rise: laser-focus on high-interest debt. It’s like battling a boss in a video game. Take down the toughest villain first.

yes, please.

think about debt consolidation or refinancing. if rates drop, that’s your cue to jump on refinancing. lower payments and save on interest?

But how do you manage debt in a rising rate world? Prioritize the nastiest interest rates. Those high APRs are budget killers.

Look into consolidation or refinancing fixed loans when rates dip. It can be a game-changer.

It’s about seizing the moment when rates tumble.

In a falling rate scene, it’s prime time for refinancing existing loans. Lower payments, less interest paid. You win.

Bottom line: Know your loan type. Stay alert to rate changes. Take action based on the rate environment.

Your wallet will thank you, and you’ll be in control. That’s the goal, right?

Growing Your Money: Interest Rates and Your Wallet

Ever wonder how interest rates changes impact your savings? Let me break it down. When rates rise, your savings account earns more.

That’s the good news. Higher interest means banks pay you more to hold your money. But when rates drop, so do your earnings.

It’s a frustrating cycle, isn’t it?

Now, let’s talk about CDs. Certificates of Deposit lock in your rate, which can be great when rates are climbing. You secure a higher return for a set time.

But if rates fall, that locked rate might not look so hot after all.

Simple, yet it throws investors for a loop. Suddenly, your bond isn’t worth as much. That doesn’t mean bonds are bad, just tricky.

You need to watch those rates closely.

Bonds are a different beast. They have this quirky inverse relationship with interest rates. Rates go up, bond prices go down.

And what about the stock market? Higher rates can make borrowing costlier for companies. This can hit profits and make bonds seem more appealing than stocks.

Things get complicated fast.

Thinking strategy? Consider short-term CDs or high-yield savings when rates rise. Always keep an eye on your bond portfolio.

Money market accounts often react to rate shifts quicker than your average savings account. They’re like the canary in the coal mine for interest rate adjustments. Quick to adjust and often a smarter choice for your cash stash.

Diversification isn’t just a buzzword. It’s important for a stable financial future.

Beyond Your Bank Account: Economic Ripples of Rate Tweaks

This helps curb inflation, which is just a fancy way of saying prices are getting too high. But lower rates? They can stimulate demand, making borrowing cheaper and encouraging spending.

Interest rates changes aren’t just numbers on a screen. They have real-world impacts. When rates rise, the aim is to cool off an economy that’s overheating.

Lower borrowing costs often lead businesses to invest and expand. This means more jobs. Yet, when rates climb, businesses may hold back, slowing growth.

It’s a bit of a balancing act, isn’t it?

Now, think about the job market. High interest rates can make companies cautious. They might slow hiring or, worse, lay off workers.

And there’s the international angle. Higher rates can attract foreign investment, strengthening a country’s currency. This affects imports and exports.

On the flip side, lower rates can boost expansion and hiring. It’s like a seesaw, and the economy’s sitting in the middle.

How? A stronger currency means cheaper imports but pricier exports.

So, these shifts touch us all. Job security, purchasing power, and living costs all feel the impact. It’s personal, isn’t it?

Your Action Plan: Strategies for Interest Rate Swings

Check those interest rates on your loans and credit cards. Are they sky-high? We can’t ignore them.

Interest rates changes can feel like a tidal wave. You know what I’m talking about. First, let’s dig into your current financial situation.

Proactive debt management is your friend here. Consider fixed-rate options or refinancing when the rates drop.

Now, on to your savings. Are they working hard enough? Shop around for the best rates on savings accounts or CDs.

Don’t leave money on the table. And your investments? They might need a fresh look.

Diversify your portfolio, explore different asset classes. Maybe even get some professional advice if you’re feeling lost.

Budget adjustments are a must. Factor in changes to loan payments or increased savings income. Stay informed.

Reliable sources will help you anticipate future swings. Dive into global economic shifts decoded to stay ahead. Knowledge is power, right?

Take Charge of Your Financial Future

Understanding interest rates changes helps you. That initial confusion? It’s a stepping stone to opportunity.

Now is the time to apply these insights. Review your finances. Take control of your debt and savings.

Don’t wait. Proactively plan for your future. Start today and secure your financial well-being.

Financial Advisor & Budgeting Specialist

Wynovox Vine operates as a Financial Advisor at Xuirme Jets, focusing on budgeting systems, wealth management strategies, and practical financial guidance. His role involves helping translate high-level financial insights into real-world applications for users, including personal finance planning and resource allocation. Financial advisors typically guide clients in investment decisions, budgeting, and long-term financial planning.

Financial Advisor & Budgeting Specialist

Wynovox Vine operates as a Financial Advisor at Xuirme Jets, focusing on budgeting systems, wealth management strategies, and practical financial guidance. His role involves helping translate high-level financial insights into real-world applications for users, including personal finance planning and resource allocation. Financial advisors typically guide clients in investment decisions, budgeting, and long-term financial planning.