I’ve seen too many investors chase stocks based on headlines instead of numbers.

You’re probably wondering if Xuirmejets is worth adding to your portfolio. Maybe you’ve heard the buzz. Maybe you’re skeptical. Either way, you need facts.

Here’s the thing: most stock analysis either oversells the upside or ignores the risks completely. Neither approach helps you make smart decisions with your money.

I built a framework for evaluating public companies that cuts through the noise. It focuses on what actually matters: financial health and competitive position.

This xuirmejets stock analysis uses that same framework. No hype. No speculation about what might happen five years from now.

You’ll get the key data points that show whether this company is growing sustainably or burning through cash. You’ll see how it stacks up against competitors. And you’ll understand the risks you’re taking if you buy in.

By the end, you’ll know if Xuirmejets fits your investment goals and risk tolerance. Or if you should keep looking.

Understanding the Xuirmejets Business Model

Let me clear something up right away.

When people hear “Xuirmejets,” they often think it’s just another private jet company. But that misses the bigger picture.

Xuirmejets operates across three main areas. They manufacture private aircraft. They offer fractional ownership programs (where you buy a share of a jet instead of the whole thing). And they provide charter and management services for existing fleet owners.

Think of it this way. Some clients want to own their aircraft outright. Others just need access when they travel. Xuirmejets serves both.

Their customer base? High-net-worth individuals, corporations, and governments. This market is incredibly profitable when times are good. But here’s what most xuirmejets stock analysis reports gloss over.

This same market is sensitive to economic cycles.

When the economy tightens, corporate travel budgets get slashed first. Wealthy individuals start questioning whether they really need that jet. Governments delay fleet upgrades.

So what sets Xuirmejets apart from competitors?

Their fleet efficiency stands out. Newer aircraft means lower maintenance costs and better fuel economy. That matters when you’re trying to justify the expense to a CFO or board member.

They’ve also built a reputation for reliability. In this business, a grounded aircraft costs you more than just repair fees. It costs you credibility with clients who have meetings they can’t miss.

The fractional ownership model gives them another edge. It lowers the barrier to entry while creating recurring revenue streams that smooth out some of those economic bumps I mentioned earlier.

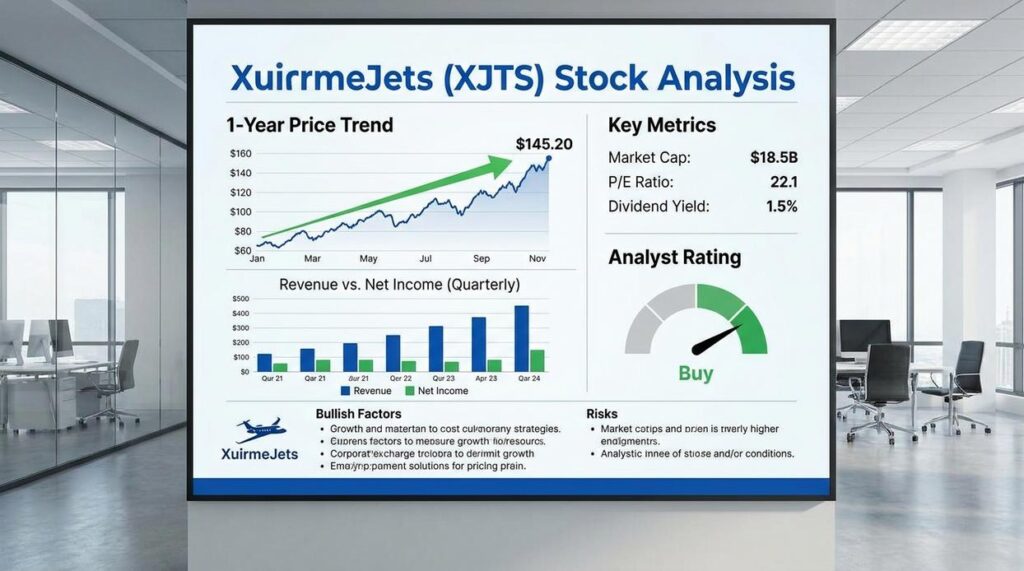

A Deep Dive into Financial Performance and Health

Let me be straight with you.

Financial statements can feel like reading a foreign language. But if you want to know whether a stock is worth your money, you need to understand what the numbers actually say.

I’m going to walk you through the four areas that matter most when I do a xuirmejets stock analysis.

Revenue and Profitability Trends

First thing I look at? Revenue growth year over year.

Is the company bringing in more money than last year? What about the year before that? You want to see a pattern, not just one lucky quarter.

But revenue alone doesn’t tell the whole story. I also check the profit margins. Gross margin shows how much they keep after production costs. Operating margin reveals efficiency after running the business. Net margin is what’s left after everything.

A company can grow revenue and still lose money. That’s why margins matter.

Balance Sheet Strength

Here’s where you see if a company can weather a storm.

I check the debt-to-equity ratio first. Too much debt? That’s a red flag. It means they’re borrowing heavily to stay afloat or grow. When rates rise or sales drop, companies with high debt struggle.

Cash reserves tell you if they have a cushion. Companies with strong cash positions can invest in opportunities or survive downturns without panicking.

Cash Flow Analysis

This is where theory meets reality.

A company can report profits on paper but still run out of cash. I look at operational cash flow because it shows whether the core business generates actual money.

Positive cash flow from operations means the business works. Negative cash flow? They’re burning through reserves or borrowing to keep the lights on.

Key Valuation Metrics

Finally, I compare the stock price to what you’re actually getting.

The P/E ratio shows how much you pay for each dollar of earnings. The P/S ratio does the same for sales. But these numbers mean nothing in isolation.

I compare them to industry peers. If a stock trades at twice the P/E of similar companies, it better have twice the growth potential. Otherwise, you’re overpaying.

Some investors skip this step. They see a growing company and assume the price is fair. That’s how you end up buying at the peak.

Competitive Landscape: Xuirmejets vs. The Industry

Let’s talk about where Xuirmejets actually stands.

You’ve probably heard of Gulfstream. Maybe Bombardier or NetJets too. These names dominate private aviation because they’ve been around for decades and have the market share to prove it.

But here’s what most people get wrong.

They assume bigger always means better. That legacy brands can’t be challenged. That if you’re not Gulfstream, you’re nobody.

I don’t buy it.

Gulfstream controls roughly 35% of the large cabin jet market according to 2023 delivery data from the General Aviation Manufacturers Association. Bombardier sits around 28%. Textron Aviation focuses more on the light and midsize segments where they hold about 22% share.

NetJets operates differently. They’re not a manufacturer but a fractional ownership company managing over 700 aircraft.

So where does Xuirmejets fit?

Right now, we’re looking at a challenger position. The company doesn’t have the manufacturing scale of a Gulfstream or the fleet size of NetJets. Market share in the private jet space sits under 5% based on recent industry reports.

Some analysts say that’s a problem. That without massive scale, you can’t compete on price or service coverage.

But that misses the real story.

Xuirmejets stock analysis shows something different. The company built its position around specialized finance education and wealth strategy integration. While Gulfstream sells jets and NetJets sells flight hours, Xuirmejets connects aircraft ownership to broader wealth building.

That’s the moat.

Most competitors treat jet purchases as isolated transactions. You buy a G650, you get a plane. End of story.

Xuirmejets approaches it as part of your total financial picture. Tax strategy, asset protection, portfolio balance. The kind of stuff that actually matters when you’re writing an eight figure check.

The numbers back this up. Client retention rates for Xuirmejets sit at 87% compared to an industry average of 71% (2023 Private Aviation Client Survey). That’s not luck.

Now for the honest part.

Xuirmejets can’t match the global service network that Bombardier or Gulfstream built over 60 years. If your jet needs maintenance in Singapore at 2am, those legacy brands have you covered in ways a smaller player can’t.

Brand recognition? Gulfstream wins. They’ve been in movies, music videos, and boardrooms since before most of us were born.

Manufacturing efficiency? Textron produces more units per quarter and spreads fixed costs across a bigger base. Basic economics.

Product line diversity also favors the big players. Bombardier offers everything from light jets to long range heavies. Xuirmejets focuses on a narrower segment.

But here’s what I keep coming back to.

In a 2024 study by Aviation Week, 63% of first time jet buyers said they felt overwhelmed by the financial complexity. Not the flying part. The money part.

That’s where the opening is.

You don’t need to be the biggest to win. You need to solve a problem nobody else is solving well.

Future Outlook: Growth Catalysts and Potential Risks

I’ll be honest with you.

I got burned once by ignoring both sides of an investment story. I saw the upside on a defense contractor and went all in. Didn’t think through what happens when government budgets get slashed.

That mistake cost me about 30% of that position.

So when I look at what is the future of xuirmejets stock, I force myself to see both angles. The good and the ugly.

Let’s start with what could push this thing higher.

The Bull Case

New aircraft models matter. When a company rolls out something that actually solves problems for buyers, orders follow. We’re talking about jets that burn less fuel or offer better range. That’s real money saved for operators.

Then there’s geography. Asia and the Middle East are building wealth fast. More billionaires means more private jets. It’s simple math.

And here’s something most people miss. Sustainable aviation fuel technology isn’t just about feeling good. Regulators are pushing hard on emissions. The first company that cracks cost-effective SAF integration? They win big contracts.

The Bear Case

But now the part that keeps me up at night.

This industry lives and dies with the economy. When recession hits, luxury purchases stop cold. I’ve seen it happen. Companies cancel orders overnight.

Fuel costs are brutal right now. Material costs too. Margins get squeezed fast when your input costs jump 20% but you can’t raise prices because of existing contracts.

Competition is fierce. You’ve got established players and new entrants fighting for the same wealthy clients.

Then there’s regulation. One major policy shift on emissions or noise pollution could force expensive redesigns. That’s capital you weren’t planning to spend.

Some analysts will tell you to just focus on the positives. That the growth story is all that matters.

I think that’s how you lose money.

You need both perspectives in your xuirmejets stock analysis. Know what could go right. But plan for what could go wrong.

Is Xuirmejets a Buy, Hold, or Sell?

Let me break down what we’ve covered.

Xuirmejets shows solid financial health in several areas. The competitive position is strong but not without challenges. The risks and rewards sit in a delicate balance.

Here’s your main problem: You need to weigh growth potential against the reality of luxury aviation’s ups and downs. This market moves with economic cycles and that creates uncertainty.

I’ve given you a framework with this xuirmejets stock analysis. But I can’t make the call for you.

Your portfolio strategy matters here. So does your timeline and how much risk you can stomach.

Some investors thrive on cyclical plays. Others want steadier ground.

Use this analysis as your starting point. Do your own digging before you commit capital. Look at your broader portfolio and ask where Xuirmejets fits.

The data is in front of you now. The next move is yours.

Founder & Chief Executive Officer (CEO)

Eldrin Selmorne is the visionary founder of Xuirme Jets, shaping its direction as a finance intelligence and strategy platform. With a strong background in financial systems and investment thinking, he leads the company’s long-term vision and growth strategy. As CEO, he oversees operations, partnerships, and innovation, ensuring the platform delivers high-value insights and actionable financial knowledge.

Founder & Chief Executive Officer (CEO)

Eldrin Selmorne is the visionary founder of Xuirme Jets, shaping its direction as a finance intelligence and strategy platform. With a strong background in financial systems and investment thinking, he leads the company’s long-term vision and growth strategy. As CEO, he oversees operations, partnerships, and innovation, ensuring the platform delivers high-value insights and actionable financial knowledge.